Carbon-free transportation is key in limiting global warming to less than 2 degrees Celsius. And for Africa, it is an opportunity for economic development and alleviating local air pollution. Africa is the fastest urbanizing region on the planet, which places strain on existing infrastructure, particularly in the transportation and energy sectors. Transportation in Africa is still primarily fossil fuel-based, which has significant economic and public health costs.

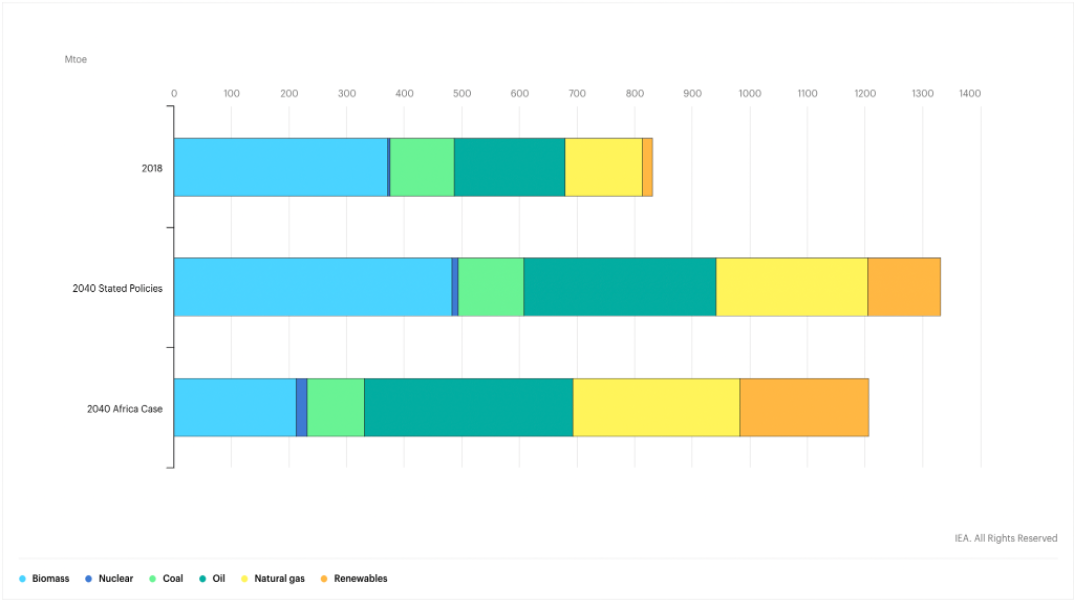

FIGURE 1. African energy consumption

Emissions aren’t just related to the number of cars on our roads, but also to the age of those cars. Vehicles in African countries are often older than those in other parts of the world – the average age of the fleet in Nigeria is about 16 years (about 5 years older than in the U.S. and E.U). Older vehicles use fuel less efficiently, which leads to increased financial strain for owners, greater fuel shortages, and poorer air quality.

Africa has an opportunity to improve economic, environmental, and social conditions by becoming a meaningful player in the emerging electric vehicle (EV) market. In 2019, the transportation sector accounted for 31% of Africa’s greenhouse gas emissions (GHG). EV deployment could also potentially remove the need for expensive petroleum subsidies.

But Africa is being left behind in the EV transition: South Africa is the current leading market for EVs in Africa. Yet in 2020, there were just 6,000 EVs on South African roads and all EVs, including hybrid models, accounted for less than 0.2% of new car sales. In Kenya, another major potential market, EVs only account for an estimated 350 of the country’s 2.2 million cars.

The vast majority of growth in EV deployment is in countries like the U.S., China, and European markets, and Africa isn’t currently on track for an equitable share in global investment. Without concerted efforts, African countries will continue to fall further behind.

The case for a homegrown African EV manufacturer

Founding a competitive, large-scale African EV manufacturer would be a critical step to bringing the EV revolution to Africa. Importantly, this would give agency to African people and prevent further reliance on international imports. Some start-ups like Ampersand in Rwanda, or Roam (Obipus) in Kenya have started working in specific niches (motorcycles and bus conversions, respectively), but to date, no large-scale African EV manufacturer exists.

A competitive African EV manufacturer could:

- Create jobs and build local industry. Homegrown EV manufacturers can reduce imports, create jobs, and build the local capital base. The jobs they develop are relatively high-paying, offer entry into the formal economy, and increase entrepreneurial opportunities for women. Affordable and available transportation also has positive impacts on the broader economy by increasing accessibility.

- Reduce the cost of vehicles. Importation tariffs on vehicles in Africa can be extremely high; in South Africa, the effective duty rate reaches 34%. By leveraging the African Continental Free Trade Area (AfCFTA) to avoid this, and limiting transportation costs by manufacturing in-country, vehicle prices could be brought down significantly. Stellantis, an international company, has sited one of its EV factories in Morocco, but a domestic manufacturer could further reduce costs by leveraging local talent and vertically integrating operations.

- Offtake used batteries to be recycled into cheaper models. The global EV market continues to grow rapidly and an African manufacturer could benefit from the increasing need to recycle batteries from the U.S., Europe, and China that are at “end of life.” Used EV batteries could retain more than two-thirds of their usable energy storage, which would be sufficient for many emerging market uses. This could be a win-win for the environment and African buyers as it would make manufacturing EVs much more affordable by avoiding the need to make batteries from scratch or compete with richer markets for a high-demand product. Tesla and Volkswagen, for instance, may even pay African manufacturers to take used batteries or sell them for a very low price rather than invest in materials recycling.

- Design vehicles based on African needs, instead of importing vehicles designed for other markets. For example, China exports vehicles to Africa that don’t meet its own safety/crash standards and in the U.S. and Europe, manufacturers tend to over-engineer vehicles for more developed contexts, such as Germany. A competitive African EV manufacturer would build for local context.

- Accelerate the transition to EVs. A local manufacturer would showcase a vision for industrial development that might enhance government conviction in limiting or banning secondhand and gray market imports.

History of EV manufacturing on the continent

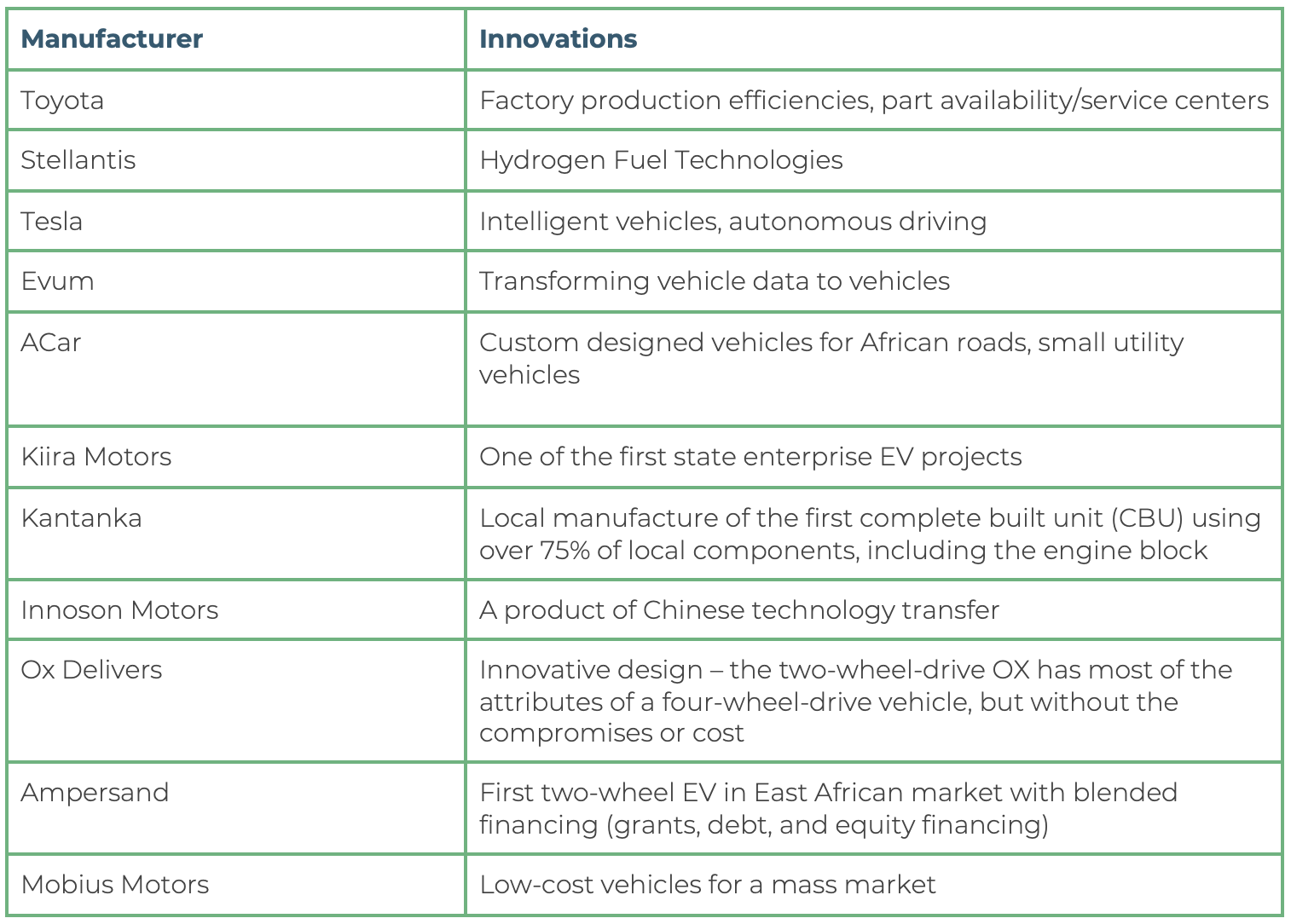

While companies like Toyota, Stellantis, Renault, and Volkswagen have been in Africa for decades, there have been few EV manufacturers on the continent to date. Recently, global car giants, including Japan’s Toyota and Germany’s Volkswagen Group, have stepped up efforts to enter the African EV market, and Stellantis and Tesla placed part of their manufacturing supply chain in Morocco in 2021. A German effort in Africa by Evum also attempted to build an EV called the ACar. Local players including Kiira Motors of Uganda, Ghana’s Kantanka, and Nigeria-based Innoson Motors are making a push to enter the market but are struggling with the high barriers to entry and poor infrastructure.

TABLE 1. History of EV manufacturers in Africa

As Africa becomes more affluent, traditional OEMs will continue to set up technical, manufacturing, and design centers. However, Ox Delivers is the most notable ongoing effort for ground-up solutions. Their work in East Africa focuses on advancing policies around infrastructure and taxes on used vehicles in an effort to take a more context-specific approach, rather than replicating western models. Mobius Motors, based in Kenya, is a major player in the 4-wheel market. They got started 10 years ago but remain limited by access to capital and high infrastructure costs.

Key challenges for the EV industry in Africa

Most African automotive manufacturing is in South Africa. However, Morocco has recently emerged as a hub, with Kenya and Egypt trailing close behind. Recently, Nigeria began investing in its domestic manufacturing capacity but has a long way to go before it can be a global producer due to inconsistent energy access and a lack of technical expertise.

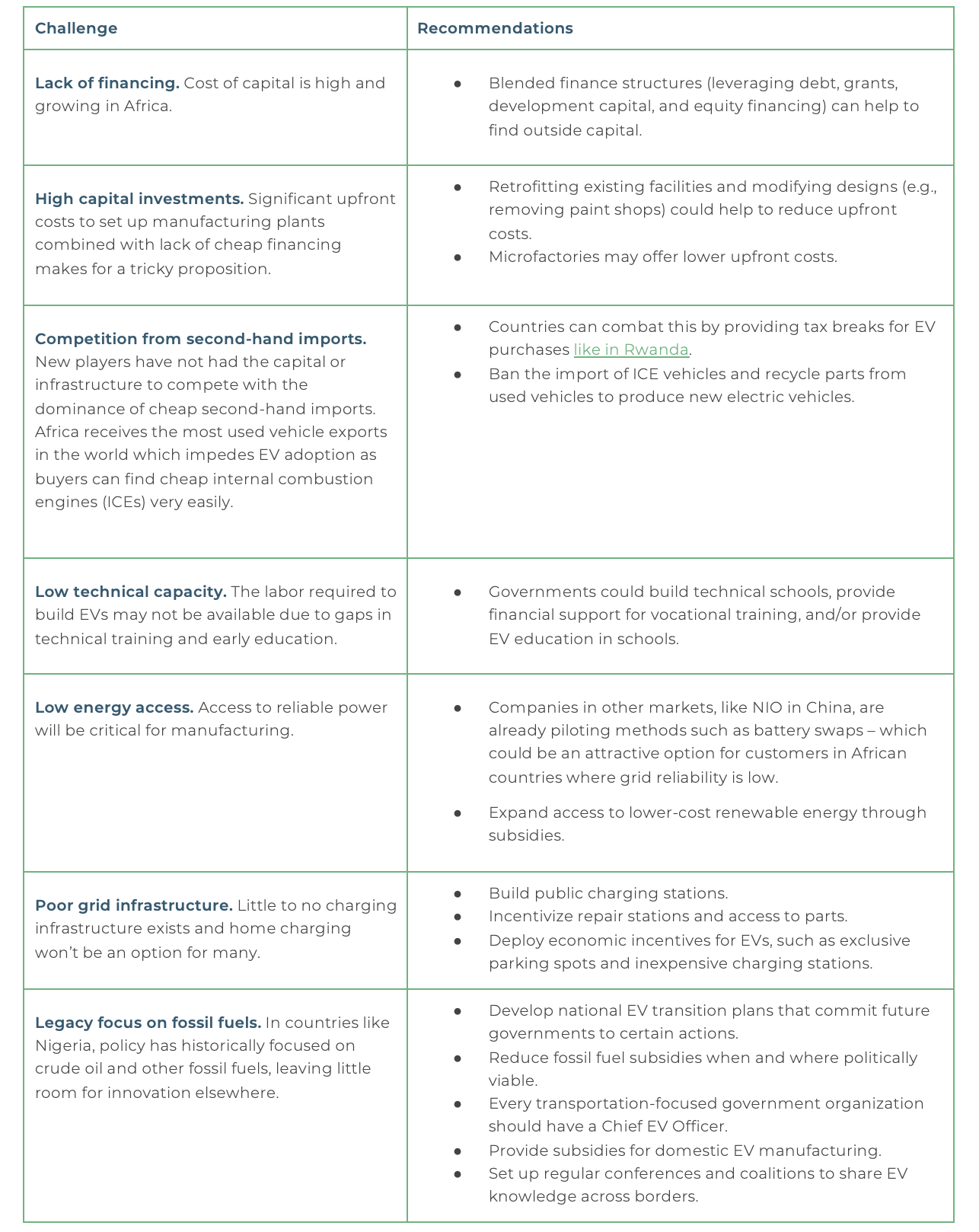

To be successful in the African market, an African EV manufacturer will have to address key challenges, such as those listed in Table 2.

TABLE 2. Key Challenges of Setting up an African EV Manufacturer and Recommendations

Market dynamics

Traditional OEMs have a stranglehold on the automotive market, due largely to high costs, supply chain (part availability), and brand recognition. The cost of EVs typically far surpasses the average earnings of even middle-class buyers in Africa. OEMs like Renault have done well to get to a competitive price point with their Dacia model by stripping away unnecessary features to make it affordable for African buyers.

Historically, OEMs designed vehicles to an abstract global standard or a one size fits all model, because design development costs are high and variation degrades economies of scale. This orientation towards a global norm led to a product mismatch in Africa. Most vehicles are not particularly suited for shared applications, harsher environmental conditions, or poorer road quality that characterize many African markets. Instead, U.S. and European models often emphasize high speeds and expensive materials and features. This is unlikely to change in the short term because large, international OEMs are unlikely to invest heavily in Africa-specific models when the current market size is so small. This creates an opportunity for potential local players.

Most African owners opt to purchase vehicles like Toyotas because they know that when the vehicle breaks down they will be able to repair it. This is incredibly important in countries where people rely on their vehicles for their livelihoods. Traditional OEMs like Toyota have done a terrific job of making parts available to all of their distributors.

Game Plan: Logistical Considerations for setting up an EV factory

Sizing and Siting the Factory

- Proximity to labor. Building factories in close proximity to population centers is an important consideration for a competitive EV manufacturer to ensure that employees can get to and from work as necessary. In Africa, this means most likely siting a factory in at least a mid-size city with some capacity for technical workforce development.

- Size: Mega or Micro? Traditional automotive factories around the world have had mixed impacts on the local communities. The prototypical factory produces 100,000-300,000 units per year with a few thousand local employees, but this can create economic overreliance on one employer to keep the local economy thriving. Larger factories require huge capital investments.

- An advantage for Africa. Smaller factories that produce 10,000-20,000 units avoid the supplier challenges that come with manufacturing at scale. In Africa, this distributed model could also help to spread workforce development more broadly and allow factories to be as close to customers as possible in order to mitigate currency and regulatory changes. Further, a distributed and modular approach could allow for collective funding and stewardship of factories across stakeholders.

Form Factor

Consumer vehicles have two-, three-, or four wheels. Two-wheelers and three-wheelers are easier to electrify and, to date, have more traction in East Africa and other emerging markets due to their affordability, availability, and flexibility. For instance, two-wheeler and three-wheeler EV sales in India are incredibly high.

In Latin America, where incomes are higher, preference for two- and three-wheelers aren’t as strong. When GDP per capita gets to $5000, the market for four-wheelers grows in a meaningful way. Two- to three-wheelers are better for low-cost production and low-income countries. For an African EV manufacturer, it could make sense to focus primarily on two- and three-wheeled vehicles, and transition to four-wheeled vehicles in richer areas and as incomes grow.

Supply chain

The main supply chain consideration is sourcing components or raw materials. The supply chain for a vehicle is large, especially for EVs given the batteries and computer chips they require. Computer chips will almost certainly need to be sourced abroad, likely from China. However, batteries have several potential sourcing options.

- Manufacture batteries. Lithium, nickel, and cobalt are the key metals used to make EV batteries. Lithium is primarily sourced in Australia, Chile, and Argentina, nickel from Indonesia, and cobalt in the Democratic Republic of the Congo. Analysts believe there is a potential shortfall in the global mining capacity required to extract the minerals needed to manufacture sufficient batteries to meet projected EV demand. But African firms might have difficulty outbidding competitors for raw materials due to high costs and the entrenched relationships that miners have with established manufacturers.

- Purchase batteries. Batteries could be imported directly from manufacturers in China and elsewhere. To provide cost-savings, second-hand batteries could be purchased at low cost (or even for a fee) from the U.S. and EU.

Manufacturing and Assembly

After sourcing the raw materials, manufacturers need to refine them into things they can use, manufacture, and assemble them. While there are a few homegrown precision metal manufacturing companies in Ghana and South Africa, imports from China currently fill most of the need for precision metal components in Africa. Some of the cost of refining can be borne by the manufacturer themselves if there are no convenient low-cost options nearby.

Scaling

Once manufacturers prove viability and product market fit (PMF), the next challenge is to manufacture at scale. Even after taking a product to market, ongoing tests are necessary including CAD design testing, digital testing, parts built, vehicle building, and safety testing to ensure the vehicle meets applicable standards. Quality control is critical during this stage and beyond.

What would it take to start a competitive African EV manufacturer?

Blended Finance for High Upfront Costs

Setting up a competitive EV manufacturer is a costly endeavor. Stellantis’ Morocco factory cost about $650M, but factories frequently exceed $1B. Vehicle design and distribution will also carry significant costs.

Manufacturers like Tesla in the US and BYD in China have leveraged generous support from government sources for start-ups. But government financial support will be limited in Africa, which means a startup will need to seek a blended finance model of debt and equity financing from sources including multilateral development banks, local banks, foreign direct investment (FDI), foreign private investment (i.e., FDIs own a controlling stake in a company by investing in its physical assets while FPIs invest only in financial assets), local government, and private capital domestic and abroad. For example, Ampersand in Rwanda got its funding from venture capital and the United States International Development Finance Corporation.

Potential cost-savings

- Remove the paint shop. A typical factory has four parts: operations stamping or the stamping of raw metal, welding the vehicle shell, the paint shop for exterior design, and general assembly where the various components are combined. Typically, the paint shop drives 50% of the total cost. is driven by the paint shop. Startup company Arrival recognized this and dramatically reduced costs by removing the paint shop entirely. Similarly, African EV manufacturers could forgo the aesthetic focus of traditional OEMs and dramatically lower the cost of the factory CapEx. to facilitate the creation of lower-cost EVs.

- Context-specific designs. Building with more contextual and locally driven design practices could help to reduce the cost of parts and, auxiliary features, and potentially lower labor costs.

- Partnerships. Partnerships, for instance with foreign EV manufacturers for the procurement of used batteries, local mining facilities for access to lower-cost materials, and/or with labor marketplaces/schools, could reduce operational costs.

Local Capacity for Personnel needs

Manufacturing should be placed near low-cost, skilled labor. In Africa, there are already people building vehicles across form factors as well as large pools of young, unemployed people who can be trained for these activities through apprenticeship, mentorship, and vocational schools set up in strategic locations. While this will require upfront investment, it will ultimately drive network effects and cost reductions as more experienced workers train new waves of employees. Further, EV manufacturers can lean on adjacent domestic manufacturing industries within and across the continent (e.g. Lagos, Cape Town, Nairobi, Cairo, Johannesburg). The technical aspects of platform design to manage the fleets and other key modules will require software expertise as well.

Government support for a nascent industry

Every successful EV manufacturer in rich countries has received significant government support, and countries like the US are deploying generous demand subsidies. We can assume an African EV manufacturer will require a similar level of start-up support. Three specific policies to do so are:

- Guaranteed access to reliable power in industrial parks.

- Preferential tax incentives and tariff treatment for imported components.

- Government-supported vocational training for the labor force.

Conclusion

In more developed markets, existing auto manufacturers are highly entrenched, and it’s difficult for new vehicle manufacturers to gain capital and support without demonstrating significant innovations that diversify their product.

In Africa, the market is undeveloped and ripe for entry. The mission of an EV manufacturer that serves local interest is suited to a continent with widely different cultures, people, and needs. Many buyers are already in favor of cleaner modes of transport and more job opportunities.

Each market within Africa will need to be studied independently but the key drivers of market selection are proximity to demand, capital location, and labor availability.

References

https://www.csis.org/analysis/urbanization-sub-saharan-africa

https://theconversation.com/electric-vehicles-in-south-africa-how-to-avoid-making-them-the-privilege-of-the-few-183415#:~:text=There%20were%20only%206%20367,up%20with%20developments%20in%20Europe.

https://www.pwc.com/ng/en/assets/pdf/africa-energy-review-2021.pdf

https://qz.com/africa/2125089/startups-are-eyeing-kenya-as-an-african-electric-vehicle-hub/

https://www.energyforgrowth.org/memo/accelerating-electric-mobility-in-nigeria/

https://www.iea.org/reports/africa-energy-outlook-2022/key-findings

https://www.iea.org/programmes/electric-vehicles-initiative

https://www.bp.com/content/dam/bp/business-sites/en/global/corporate/pdfs/energy-economics/statistical-review/bp-stats-review-2021-africa-insights.pdf

https://europe.autonews.com/article/20130102/ANE/312259994/how-renault-s-low-cost-dacia-has-become-a-cash-cow

https://www.irena.org/-/media/Files/IRENA/Agency/Publication/2021/March/Renewable_Energy_Transition_Africa_2021.pdf

https://mobiusmotors.com/

https://todaysmachiningworld.com/magazine/african-lean-pioneering-precision-machining-in-ghana-africa/

https://europe.autonews.com/automakers/home-market-still-dream-african-automakers

https://alexmitchell.substack.com/p/sutainable-mobility-volume-10

https://www.wkbn.com/news/local-news/this-was-kinda-a-shocker-mayor-reacts-to-lordstown-motors-top-officials-resigning/

https://changing-transport.org/kenyas-e-vehicles-regulatory-environment/

https://www.africon.de/en/slide-of-the-month-sotm-july-the-age-of-vehicles-in-operation-in-nigeria/

https://www.confused.com/car-insurance/average-cars-around-the-world

https://centurionlg.com/2022/05/03/electric-vehicles-is-the-timing-right-for-africa/#:~:text=This%20revolution%20is%20only%20just,the%20country’s%202.2%20million%20automobiles.

https://businessindia.co/climatechange/women-lead-in-ev-jobs

https://energy.economictimes.indiatimes.com/news/power/job-opportunities-in-ev-sector-growing-women-climbing-to-the-top-study/92797239

https://auto.economictimes.indiatimes.com/news/two-wheelers/scooters-mopeds/electric-two-wheelers-register-a-staggering-132-growth-in-2021-but-2022-promises-to-be-even-better/88734671

https://www.afrik21.africa/en/morocco-stellantis-to-produce-its-new-electric-car-at-the-kenitra-plant/

https://www.nytimes.com/2021/04/21/business/arrival-electric-vehicles.html

https://www.researchgate.net/figure/Vehicle-ownership-as-a-function-of-GDP-per-capita-over-the-last-few-years-Source-IPCC_fig1_324389472

https://www.linklaters.com/en/insights/thought-leadership/electric-vehicle-batteries/powering-the-future/sourcing-raw-materials

https://www.ncbi.nlm.nih.gov/pmc/articles/PMC8390110/

https://www.sciencedaily.com/releases/2021/10/211007224641.htm

https://www.marklines.com/en/global/10159