Dynamic progress in Kenyan power sector has been driven by:

- Multiple rounds of power sector reforms.1

- An aggressive Last Mile Connectivity campaign and a thriving off-grid solar market, which have pushed access from roughly 20% six years ago to above 50% in 2018.

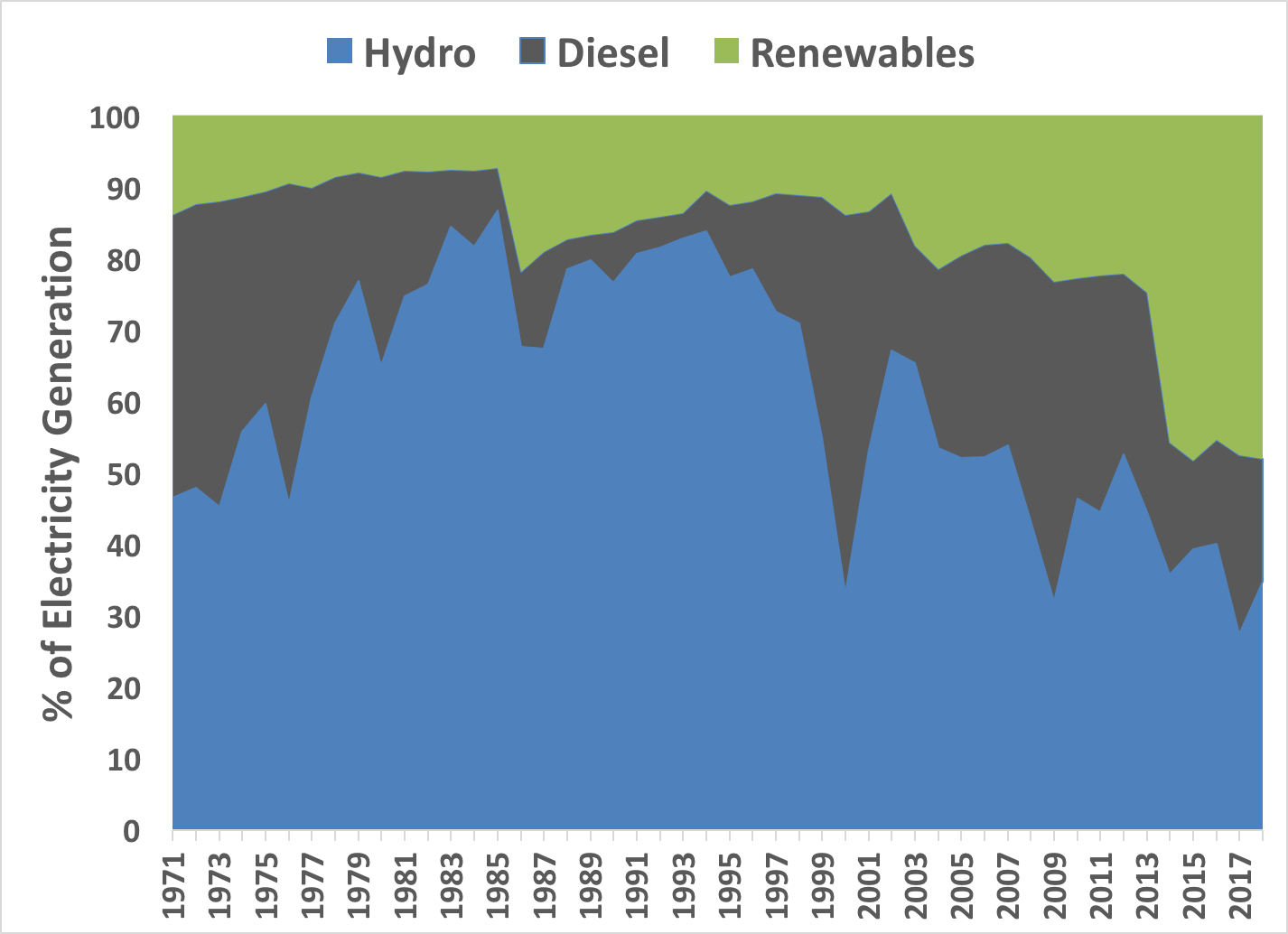

- A highly diversified power mix that includes geothermal power (now 48% of national generation) and continues to displace imported diesel and increasingly unreliable hydroelectric generation.2

- Kenya is poised to add Africa’s largest wind farm (310 MW at Lake Turkana) and the region’s largest solar facility (55 MW in Garissa).3

As a result, Kenya currently can now produce significantly more power than it consumes. This is a dramatic reversal of the crippling power rationing of the early 2000s4 and the 2010 power crisis.5

Despite this progress, many households still lack electricity, those with connections experience poor quality, while reliability stifles economic growth. Like many utilities in Africa, the Kenya Power and Lighting Company (KPLC) is beleaguered by an unprofitable customer base, mismanagement, and an often-conflicting dual mandate of access and profitability.

Despite Kenya’s progress, the sector faces 7 main threats:

1. Stagnating demand threatens the national utility. While Kenya Power’s customer base has grown from under 2 million in 2011 to over 6 million in 2017, residential customers consume very little electricity — on average 30 kWh/month per household (versus 150 in China or over 900 in the US).6 Low consumption is a symptom of stunted socio-economic development, where rural and poor populations have yet to graduate to more consumptive and productive uses of power. Low demand is compounded by the high cost of connecting new customers, who consume even less.7 This falling revenue per customer is increasingly a serious threat to KPLC’s business model. Some new balance between profitability and expanding access may need to be found.

2. The rise of captive power. Some 55% of Kenya Power revenues are from 3,600 large mostly industrial power users. These customers are starting to migrate off the grid, citing high power bills, unreliability, and attractive distributed generation options. For example, Devki Group recently set up their own coal-generation plant to power their steel and cement plants.8 The Kenya Tea Development Agency is also building small hydropower stations for its tea factories.9 Retention of these customers should be a critical priority for KPLC. Even with a recent retention effort, erosion of the industrial and commercial base is likely to continue.10

3. Reliability remains poor. While reliability data are limited, World Bank estimates show generally poor but improving performance.11 Customer dissatisfaction runs high, illustrated by the nickname “The Kenya Paraffin Lamps and Candles Company.” The World Bank-backed grid modernization program addresses some grid stability issues, but big-ticket generation projects continue to dominate investment.12 While Kenya has taken important steps to diversify its generation mix, new intermittent generation on the grid may challenge its current inflexible supply mix and limited balancing resources.

4. Consumer backlash over pricing. Efforts to experiment and reform the pricing system are laudable, but have been hampered by poor communications, uneven deployment, and confusion. KPLC routinely levies surcharges linked to oil prices and local currency fluctuations causing significant price uncertainty. Changes to billing practices have also been confusing. A tariff harmonization plan that eliminated fixed tariffs and increased variable tariffs led to higher overall charges for more than half of customers.13 The regulator has also begun offering reduced prices for night-time usage to its industrial customers with smart-meters, but the uptake has been slow.

5. Overly rosy projections drive over-investment in generation. As consumption growth has stagnated, the government has abandoned a 2013 proposal to add 5000 MW. Nevertheless, it is pushing ahead with plans to pursue nuclear generation and a 1000 MW coal plant at Lamu.14 Hopes for regional power trading might be dashed as nearly every country in the region aims to become an electricity exporter. Plans for new generation should be based on data-driven demand projections by parties without incentives to overstate growth. Overbuilding jeopardizes the already tenuous fiscal situations of utilities.

6. Corruption at Kenya Power. A recent corruption scandal and imprisonment of KPLC officials have further eroded consumer confidence, tarnished the brand, and hindered the utility.15 Customer complaints on metering, bribes, favoritism, and other issues also persist. The government has directly meddled in KPLC, such as a billing customers for backdated fuel costs accrued in the lead up to national elections in August 2017.16

7. Policy and regulatory uncertainty reigns. To better meet the needs of an evolving sector, updated energy legislation was drafted in 2015,19 but has been held up in parliament. In the interim, energy policy is largely driven by a (sometimes-inconsistent) web of aspirational national strategies, executive mandates, donor-driven proposals, and internal planning by sector players. Meanwhile, the draft energy bill proposes to create a number of new regulatory entities with potentially overlapping mandates, while there is lack of clarity over the role of newly-empowered counties. The government also needs to refine policies towards distributed generation, including transparency on utility expansion plans and policies to integrate distributed assets into the central grid. These and many other critical policy and regulatory issues with significant lock-in effects are on the table as the government revisits the question of comprehensive energy legislation this year.

Figure 1. The changing face of Kenya’s electricity mix. While droughts lead to occasional spikes in generation from imported diesel, Kenya has made an inexorable push towards a more renewable electricity supply via massive investment in geothermal electricity. (Source data: World Bank and KNBS)

Endnotes

1. Eberhard et al (2018) Kenya’s lessons from two decades of experience with independent power producers.

2. Kenya Power and Lighting Company. 2017 Annual report.

3. Kamau, M. (2018) Sh13.5 billion Garissa solar plant be commissioned in two weeks.

4. Masakhalia, F. Y. O. (2000) Statement by the Government of Kenya on the Reform of The Power Sector.

5. Burnham, M. & Groneworld, N. (2010) Droughts Turn Out the Lights in Hydro-Dependent African Nation.

6. EIA (2016) How much electricity does an American home use?

7. Moss, T. Kincer, J. (2018) Energy Access Isn’t the End of the Story: New Evidence of Electricity Demand in Kenya.

8. Njanja, A (2016) Devki Group switches on 15MW Kajiado coal power generator.

9. KTDA (2016) KTDA Signs Ksh. 5.5 BIllion Loan Agreement To Construct Seven Small HydroPower Projects.

10. Kenya Power and Lighting Company (2018) Enhancing Supply Quality to Support Manufacturing.

11. World Bank, Doing Business – Measuring Business Regulations.

12. World Bank (2015) KE Electricity Modernization Project.

13. Energy Regulatory Commission (2018) Clarification on the Reviewed Retail Electricity Tariffs for the 2018.19 Tariff Control Period.

14. Kamau, M. (2017) Demand setback now puts Kenya’s mega power plan on the back burner.

15. Menya, W. (2018) Top bosses of scandal-hit Kenya Power arrested.

16. Otuki, N. (2018) Sh8.1bn slapped on power bills.